Då har John Hussman släppt en av sina månadskrönikor igen. Som vanligt med ett negativt sentiment och som vanligt väldigt läsvärt med många bra citat.

Några av mina favoritcitat från artikeln:

In the latter stage of the bull market culminating in 1929, the public acquired a completely different attitude to the investment merits of common stocks. Why did the investing public turn its attention from dividends, from asset values, and from average earnings, to transfer it almost exclusively to the earnings trend , i.e. to the changes in earnings expected in the future? The answer was, first, that the records of the past were proving an undependable guide to investment; and, second, that the rewards of offered by the future had become irresistibly alluring.

– Benjamin Graham & David L. Dodd, Security Analysis, 1934

As Galbraith wrote of prior speculative episodes, “As long as they are in, they have a strong pecuniary commitment to the belief in the unique personal intelligence that tells them that there will be yet more.”

With margin debt at the highest level in history relative to GDP, with the most extreme valuations on record, with bullish sentiment at lopsided extremes, with the S&P 500 pushing its upper Bollinger bands at every resolution, with divergence and deterioration in our measures of market internals, and with the S&P 500 strikingly overextended relative to widely followed moving averages (e.g. 200-day), I believe that the market is at clear risk of a vertical “panic” or “air-pocket” much like we observed in 1987 and 1998. Neither of those panics was associated with a recession. They were just points where overextended investors attempted to reduce their leveraged positions into a market where the bids were insufficient to absorb the selling without large price discounts.

A 20-35% decline would easily fit into that sort of outcome. That wouldn’t bring valuations anywhere near their historical norms, but there’s really no need to make projections or rely on any given scenario. At present, we’ve got a combination of extreme valuations, unfavorable market internals, and upward yield pressures, which we’ve never viewed favorably, because it can create a “trap door” situation.

It’s worth remembering that air-pockets, panics, and crashes typically reflect a depressed and inadequate risk premium being driven higher. No other “catalyst” is needed but a brief bout of risk-aversion or profit-taking that nicks overleveraged investors enough to provoke a concerted and self-reinforcing attempt to exit.

Let’s assume that in the coming 5 years, S&P 500 revenues grow at the same 4% annual rate as in the two decades leading up to the pre-pandemic highs. Suppose that over that 5-year period, the S&P 500 price/revenue ratio retreats from its current multiple of 3.1 to a level no lower than the 2000 bubble extreme of 2.2. Given a dividend yield of just 1.4% on the S&P 500, the following average annual total return would result:

1.04(2.2/3.1)^(1/5)-1+.014 = -1.5% annually.*

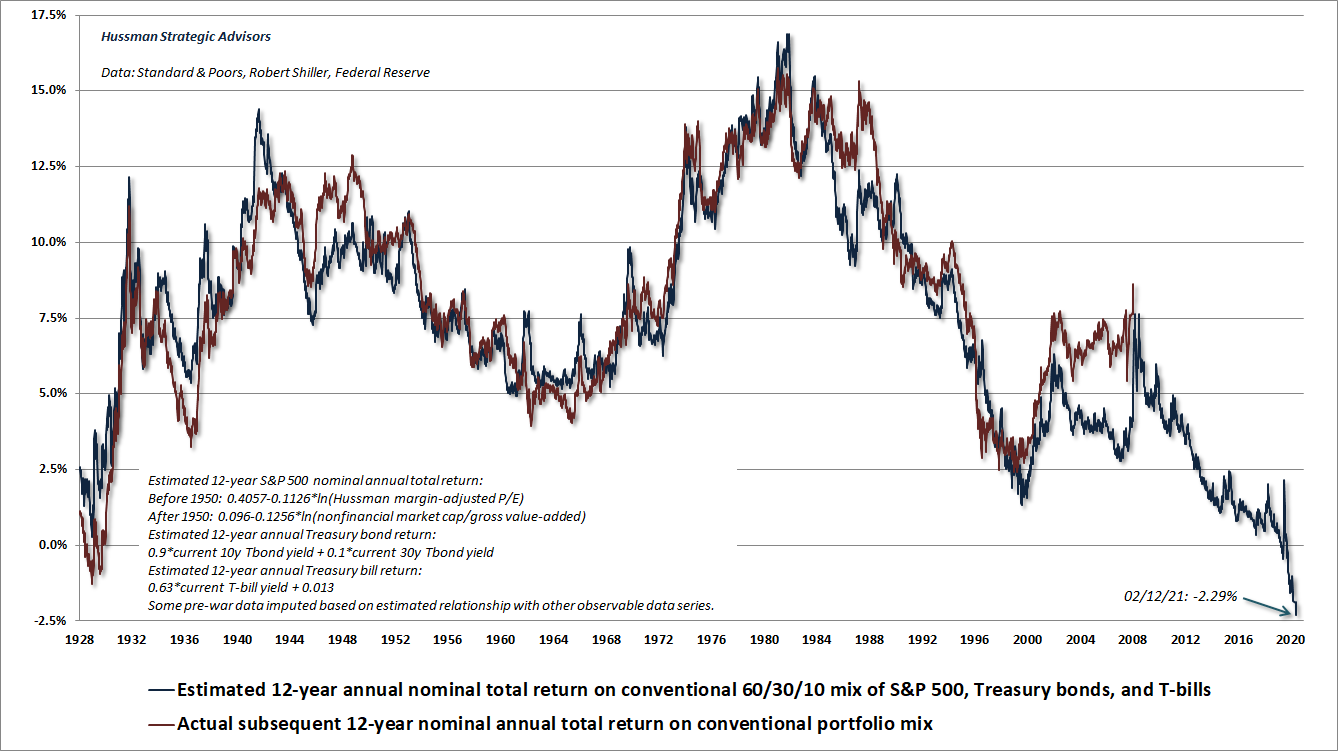

The collapse in our estimate of prospective returns for a conventional portfolio mix (60% S&P 500, 30% Treasury bonds, 10% T-bills) is the mirror image of the advance in recent years to hypervalued levels across these asset classes.

Making money in the stock market was now the easiest thing in the world. It was only necessary to buy ‘good’ stocks, regardless of price, and then to let nature take her upward course. The results of such a doctrine could not fail to be tragic.”

– Graham & Dodd, 1934

Quantitative Easing! is synonymous with The Fed! These phrases are complete and fully-articulated arguments. They don’t need data. They don’t need a ‘mechanism.’ They don’t need history. The mere words are enough. Their power to support the markets is so obvious to investors that simply referring to them is treated as a mic drop. They rest entirely and victoriously on investor psychology alone. It’s that form of QE that has helped to drive the S&P 500 to valuations that exceed the 1929 and 2000 extremes.

Because Quantitative Easing! is purely a mental formation, the only thing that alters its effectiveness is investor psychology itself . Mental formations like The Fed! and Quantitative Easing! are sufficient to amplify behavior that supports the financial markets, provided that investors are inclined to speculate – which is best gauged by the uniformity of market internals.

From this particular starting point, I expect that the S&P 500 will go nowhere for something approaching 20 years. Fortunately, even if the market goes nowhere over the coming 20 years, it will likely go nowhere in a very interesting way. Examine the period between April 1995 and March 2009. The total return of the S&P 500 did no better than Treasury bills, but the period also included two bubbles and two crashes. We’ll be just fine, as long as we draw the right lesson from recent years. The lesson isn’t that valuations are irrelevant. The lesson isn’t that prices always quickly get back to their highs. The lesson is that valuations matter, but so too does investor psychology – and we have tools to gauge and navigate both of them.

Ja, då känner man sig redo att gå och sälja alla aktier som vanligt när man läst det här. ![]()

![]()

! Sluta läsa sådana dumheter!

! Sluta läsa sådana dumheter!