Apologies for putting this up in English (still naive in Svenska). I have been following this community for a while and very grateful for all the advice shared here.

Hi everyone,

We are an expat couple (both 31 years old) based in Stockholm, one working in a bank and other for a MNC. We have a combined net income of ~78k SEK per month (excluding any benefits/ bonus/ overtime pay) and currently live via a first hand contract. Our monthly expenses are ~35% of our net income which includes everything rent, food, transport (no car), insurances, sending money to parents and so on.

Currently, we have ~450k SEK in savings/ ISK in Avanza. Just to mention, we also have investments ~200k SEK in our home country which we can pull if needed.

- What is a reasonable price to target for our first home based on our income?

- We are looking at 5M SEK apartment around 80 sq.m. (planning to put up 750k SEK as down-payment) resulting in monthly expenses (including amortization which I count as an expense due to it’s illiquidity) of ~53% based on our current income.

- We are also looking towards family planning in a year or so which would mean reduced income and savings for a couple of years.

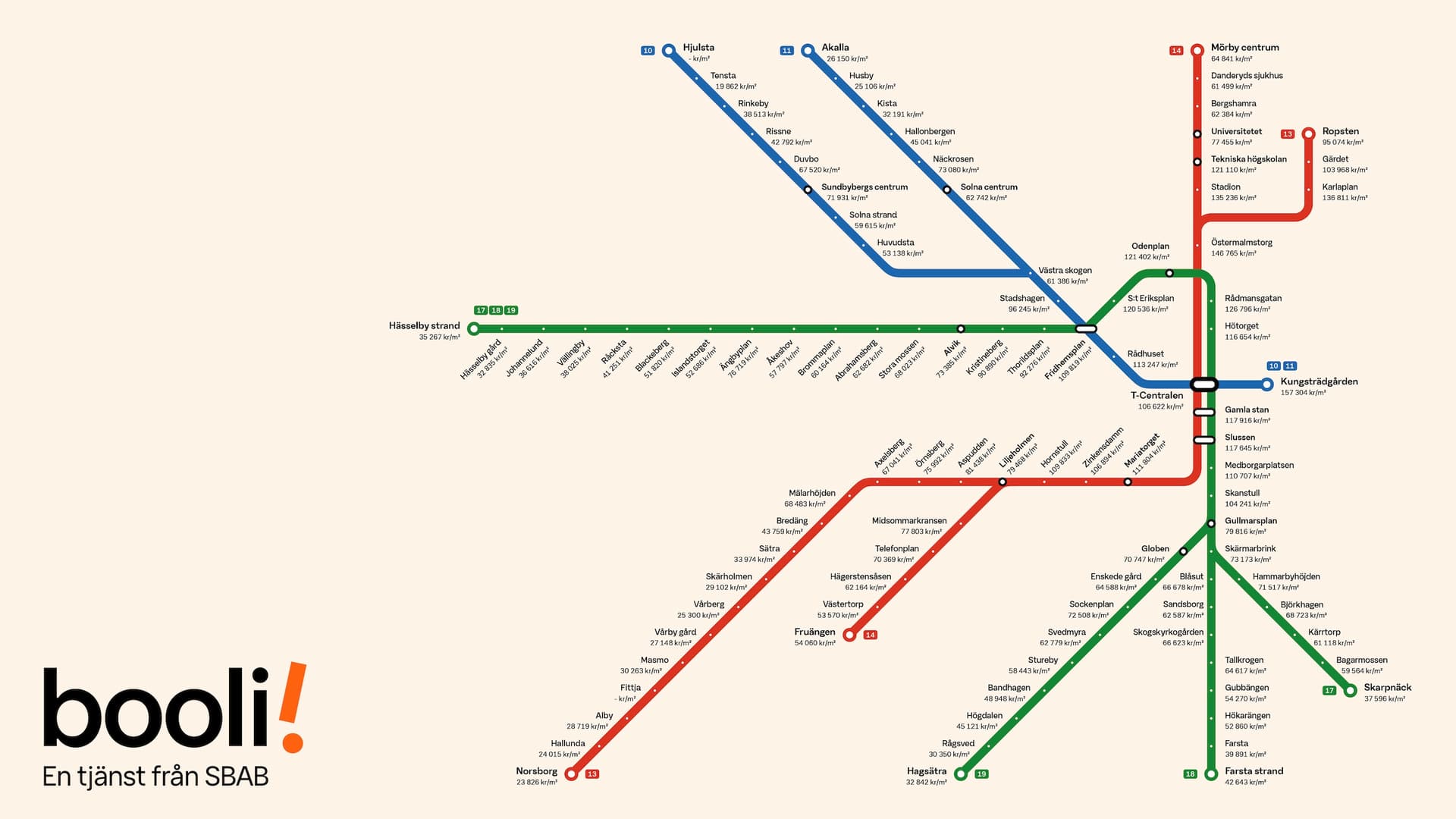

2. Any recommendations on location to consider?

- We have mostly lived in North Stockholm and both work in Solna, so prefer not too far (~30-45 minutes commute) and not too close to city centre as well

3. Considering there are upcoming policy changes related to mortgage and increase in avgift next year, any advice/ tips based on your experience?

Thanks for your time.