Rapport från Goldman “Building Long-Term Returns: Our 10-Year Forecasts”

Abstract:

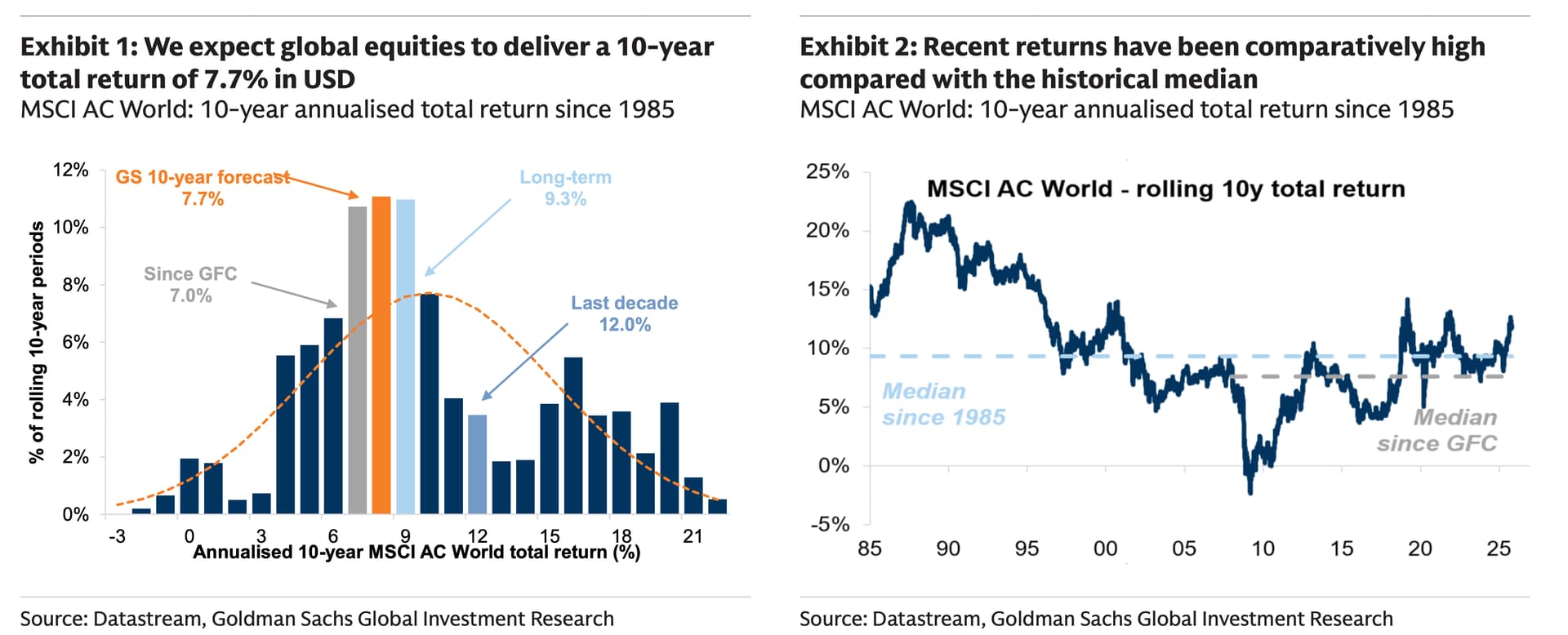

We expect global equities to deliver solid long-term returns despite elevated valuations. Our forecast of 7.7% per annum (in USD) sits close to the historical median, supported by structural drivers such as nominal growth, profitability, and shareholder distributions.

Our modelling uses a common framework across regions, adapted to local specifics.

We apply a building-block methodology where total return equals earnings growth plus valuation change plus dividend yield, with assumptions derived from top-down models incorporating local drivers and index composition.Earnings growth remains the primary engine of performance. We expect global earnings — including buybacks — to compound at roughly 6% annually. Dividends provide the rest of the return, while we expect valuations to ease modestly from current highs.

Regional outlooks highlight some dispersion:

- United States: +6.5%, driven entirely by earnings and modest dividends (while buybacks compensate for the valuation drag).

- Europe: +7.1%, half driven by earnings and half driven by shareholder return.

- Japan: +8.2%, underpinned by EPS growth of 6.0% and policy-led improvements in payouts.

- Asia ex-Japan: +10.3%, aided by ~9% EPS growth and 2.7% dividend yield, partly offset by valuation de-rating.

- Emerging Markets: +10.9%, led by strong EPS growth in China and India.

Diversify beyond the US, with a tilt towards Emerging Markets. We expect higher nominal GDP growth and structural reforms to favour EM, while AI’s long-term benefits should be broad-based rather than confined to US Technology.