Ja, jag tyckte det var en dålig artikel, Inflation för dummies ![]()

Bättre väl att försöka förklara varför det är bra att sitta med bolån nu, om bostadspriserna faller, utan att blanda in ost! ![]()

Ja, jag tyckte det var en dålig artikel, Inflation för dummies ![]()

Bättre väl att försöka förklara varför det är bra att sitta med bolån nu, om bostadspriserna faller, utan att blanda in ost! ![]()

Vart finner du att

?

Sen så ska administratören uppdatera räntan i systemet, frågar på ett forum lite snabbt och får svaret:

sudo rm -Rf /

Det är där är ju en extra förutsättning du själv har hittar på.

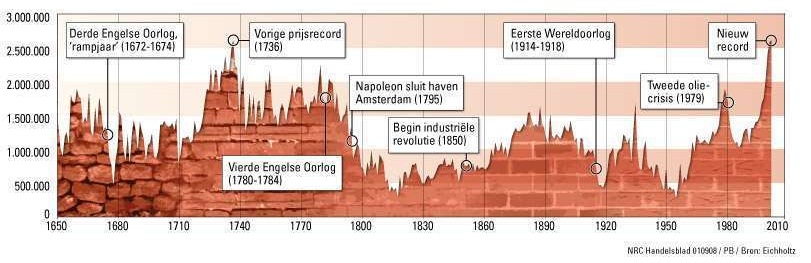

Normalt brukar man anse att bostäder följer eller ökar mer än inflationen.

Det kommer pratas utav bara fan om att “ta ansvar” då de stora fackförbunden ska komma överens med arbetsgivarna om nivåerna i nästkommande avtal… men hur ska man som förhandlare kunna sälja in löneökningar på 2,3 procent då inflationen är mer än det dubbla? Vete fan var det här slutar.

The great reset?

Great reset, self destruct, TEOTWAWKI…kärt barn har många namn

Det är spekulation från min sida. Kanske är 20 % en överdrift. Men tex i denna artikel pratas det om fallande bostadspriser på 6 %. Bostadspriserna vänder ner nästa år till följd av stigande boräntor - SBAB

Min poäng är att snacket om att inflationen äter upp bolånet bara stämmer om priset på bostaden ökar i samma takt som inflationen.

Du har rätt i att jag själv hittar på den förutsättningen. Men den är långt ifrån orealistisk, fast en 20 procentig nedgång är kanske lite väl pessimistiskt. Dock finns det ingen naturlag som säger att bostaden normalt följer inflationen.

Och vad är alternativet om prisökningarna beror på dyrare produktion?

Jag tänkte precis med på detta. Höjs räntan för mycket, kommer ju folk dra in på att “roligt” d.v.s restaurang, bio, krogen etc. och därmed större arbetslöshet och därmed mindre skatteintäkter.

Då borde man väl hamna i en form av lånkonjuktur och sedan sänka räntorna, eller tänker jag fel?

Ja, du har väldigt rätt i det du säger.

Samtidigt, så ju skuldsättningen i Sverige hög. Tänker mest i storstäderna t.ex. Stockholm och Göteborg. Vart går gränsen till folk slutar konsumera alls, och bara lägger pengar på boendet?

För mig personligen, hade jag lagt allt annat åt sidan. Sålt bilen, inte köpt kläder, inga nöjen, enbart för att få behålla bostaden.

Tror många tänker så med mig. Och då försvinner ju jobb i sin tur i t.ex. serviceyrken eller “icke-samhällskritiska” delar av den.

Ja, lågkonjunktur kommer till sist att leda till sänkta räntor enligt skolboken.

Sedan har bostäder det värde någon är beredd att betala.

I en lånedriven bostadsmarknad såsom det har varit en längre tid är det samma sak som bankernas lånelöften.

(högst lånelöfte vinner budgivningen)

Dessa är i sin tur beroende på den ränta som ligger till grund för KALP.

Jaha, jag som tänkte att jag ev. skulle amortera en stor del av mitt lån snart. I guess not?

Från dagens The Telegraph https://www.telegraph.co.uk/business/2022/05/25/davos-elites-fear-volcker-moment-central-banks-draw-swords/

Experts warn the Fed is ready to raise rates as high as 5pc – even if it results in a recession

ByAmbrose Evans-Pritchard IN DAVOS25 May 2022 • 4:55pm

The collective warning from Davos is that all-powerful central banks are no longer on your side, so don’t tempt fate by reflexively buying the dips.

The monetary gendarmes have let the inflation genie out of the bottle and will have to squeeze markets until the pips squeak in order to stop it now running wild across the major western economies.

“The ‘Fed Put’ is over. They don’t mind what happens to markets,” said Jason Furman, former chairman of the White House Council of Economic Advisers.

He warned that rates will have to go much higher than the Federal Reserve has so far admitted, or than markets are expecting.

“They haven’t done enough yet to prepare people, “ he said, speaking at the World Economic Forum.

There are mounting worries that the Fed will ultimately be forced to dish out the ‘Volcker’ medicine of the late 1970s. It has already begun to engineer a deliberate and (hopefully) controlled crash in equity and asset prices.

“I don’t think the Fed believes its own forecasts or inflation models any more, they have been so badly burned,” said Mr Furman.

The prevailing view in elite policy circles is that if the Fed fails to lance the boil now, the punishment will be even more painful and destructive later.

“It reminds me of Argentina,” said Harvard professor Ricardo Hausmann, a veteran of Latin American crises, describing the Fed’s endless series of excuses last year, even as the economy was flooded with money and inflation was clearly building up.

“There is just too much stimulus in the pipeline and they are going to have to act much more forcibly. I lose sleep thinking the Fed is way behind the curve,” he said.

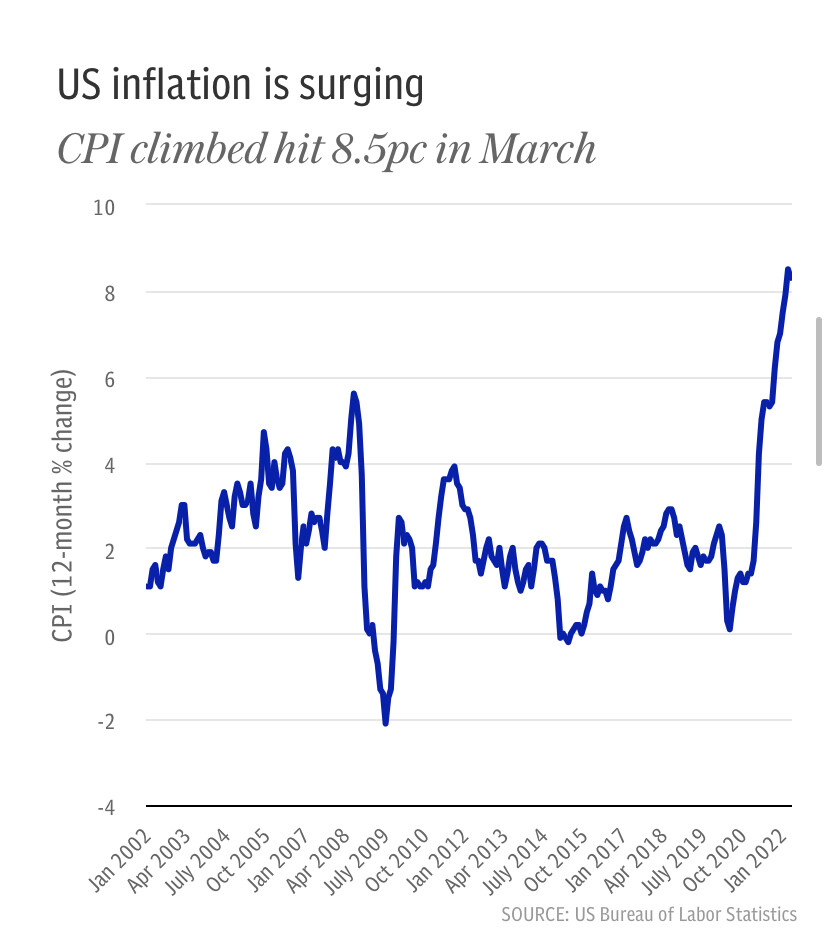

Mr Furman said that inflation is being driven first and foremost by excess demand and liquidity in the economy, rather than by supply chain disruptions or higher energy prices, as the Fed argued fervently until late last year. The institution has badly misjudged the calibration of stimulus.

It predicted inflation this year of 2.2pc as recently as December, but the figure is already running at a 40-year high of 8.5pc. The Fed staff relied on a New Keynesian Phillips Curve model that omits most of the key ingredients in price shocks and is “incapable of predicting any inflation,” said Mr Furman.

Gita Gopinath from the International Monetary Fund said that what began as a global supply shock during the pandemic has metamorphosed into something closer to a (positive) demand shock with its own self-feeding momentum, which central banks cannot safely allow to run unchecked.

“Over the last three months broad-based inflation has spilled through the global economy and we’re seeing it much more widely,” she said in Davos.

“The surprise element has been that we’ve been used, over the last decade, to living in a world where we worried about demand being too low. Then you get hit by the pandemic and you have major global supply shocks.”

It has been a nightmare for central banks to figure out where the proper balance lies between demand and supply in such a fast-moving and turbulent picture.

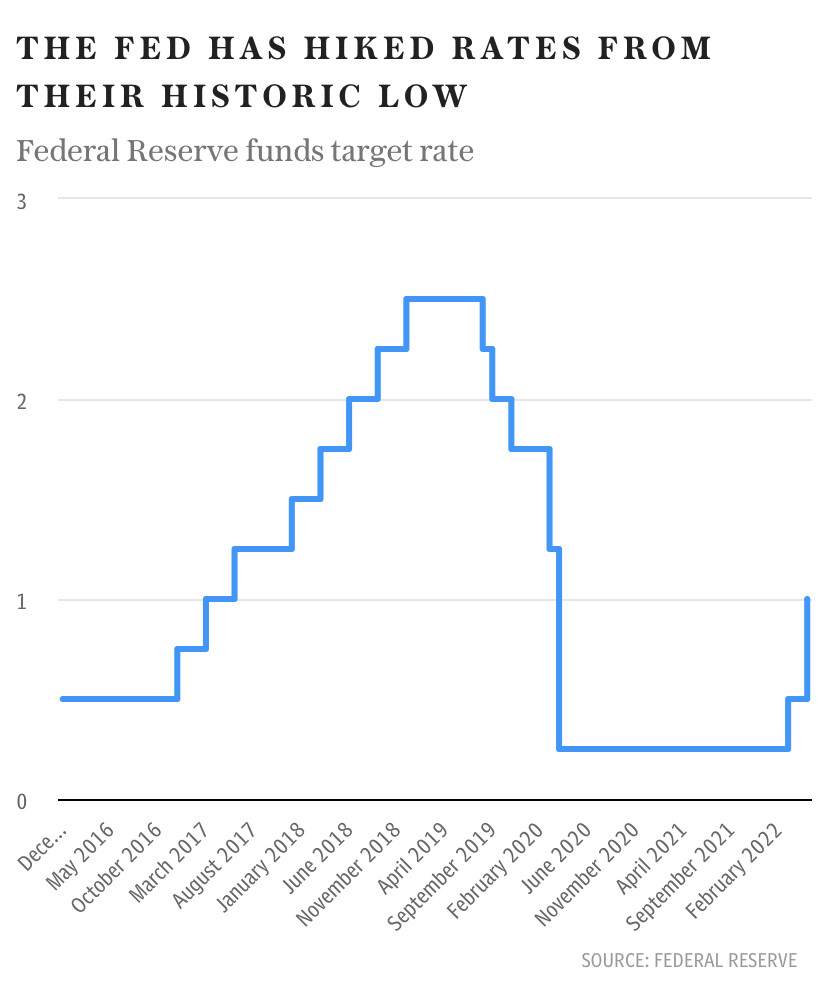

Correcting for past mistakes – or over-correcting, in the view of monetarists – the Fed now seems determined to rein in inflation whatever the economic cost. It is raising rates in 50-point chunks and has swung abruptly from asset purchases to asset sales, targeting quantitative tightening (reverse QE) of $95bn (£76bn) a month by September.

Columbia professor Adam Tooze said some are muttering sotto voce in Davos that the Fed may have “turned Frankenstein on the markets”. Having bathed investors and the owners of wealth with abundant liquidity for years, it is now targeting its monetary squeeze on the same economic elites. What QE giveth, QT taketh away.

Bill Dudley, ex-head of the New York Fed, said the institution is actively attempting to deflate Wall Street equities in order to help break the back of inflation through the mechanism of the wealth effect. It is ‘front-loading’ rate rises across the maturity spectrum with hawkish rhetoric, forcing the markets to price in tough action before it even occurs.

Even so, the Fed may not yet have gone far enough. Mr Dudley said it should come clean and admit that rates are going to 4pc or even 5pc even if that means a likely recession, rather than “sugar-coating” its message. The federal funds rate is currently still just 1pc, and markets expect it to reach 3pc by the end of the year.

Not everybody agrees that a monetary purge of such ferocity is either necessary or wise. Scott Minerd from Guggenheim Partners said in Davos that the “neutral rate” is lower than the Fed thinks, and warned that the leveraged loan market is already cracking as the economy rolls over.

Nobel economist Joe Stiglitz said higher rates might actually make inflation worse by curbing the very investment needed to repair damage to global supply chains and productive capacity.

But the doves are being drowned out by a chorus of voices demanding tough love, even in Europe where most of this year’s one-off jump in the price level is indisputably caused by an imported energy and trade shock.

Klaas Knot, Holland’s ECB governor and head of the global Financial Stability Board, said there are signs that inflation expectations in the eurozone are becoming “de-anchored”. The 10-year measure was 1.9pc last November: it was 2.4pc in May. “There is a considerable drift upwards,” he said.

“As a central bank, we’re not looking at energy prices. That is yesterday’s news, water under the bridge. But the components of underlying inflation are all going North East, and the question is where do they stop?” he said in Davos.

Mr Knot said there are early warning signs of an inflationary wage-spiral taking off in Eastern Europe, Germany, the Netherlands, and even in Spain.

He said central banks cannot do anything about an imported energy shock, calling it “futile” to tamper with the price signal. “Energy inflation is a trade loss. We have to accept that we have collectively grown poorer,” he said.

Mr Knot said targeted fiscal help for poor families can be justified as a matter of social justice but it makes absolutely no sense for governments to rush through general stimulus packages, which merely drive inflation higher. “We cannot compensate everybody,” he said.

Det skulle inte förvåna mig om räntehöjningarna i USA kommer att skörda fler offer än den pandemi vars motåtgärder (del?)orsakat nuvarande inflation.

Jag tänker att anledningen till att vi nu ser stigande inflation är den höga skuldsättningen.

För mycket pengar i systemet leder till att värdet på pengarna sjunker analogt med att saker som alla har har ringa värde medan ovanliga saker som bara ett fåtal har har ett högt värde.

Anledningen till att det finns för mycket pengar är att bankerna gladeligen skapar pengar som de sedan lånar ut och tjänar pengar på.

Bostadspriser bestäms ofta egentligen inte av bostadens faktiska värde utan av hur mycket pengar bankerna är villiga att låna ut. Bankerna bestämmer sålunda bostadpriserna och trissar upp dessa då de vill låna ut så mycket pengar som möjligt för att sedan tjäna pengar på lånets avgifter och räntor.