For retirees who seek a fixed real withdrawal from their portfolio in retirement, a starting withdrawal rate of 3.8% is safe in Morningstar’s model over a 30-year time horizon, assuming a 90% success rate (defined here as a 90% likelihood of not running out of funds) and a balanced portfolio.

That is appreciably higher than the 2021 figure, which was 3.3% for a balanced portfolio with a 90% success rate.

Employing a more aggressive equity allocation does not meaningfully improve safe starting withdrawal rates.

Investors with shorter time horizons of 10 to 15 years can employ a higher withdrawal rate if using a conservative portfolio mix than they can with a more equity-heavy one.

Dynamic withdrawal strategies may help retirees consume their portfolios more efficiently, factoring in both portfolio performance and spending, but they also add variability to retiree spending that may or may not be acceptable to the individual.

Of the dynamic strategies we tested, the “guardrails” system does the best overall job of balancing higher withdrawals alongside cash-flow-volatility considerations.

The right level of flexibility in a retiree’s spending system will depend on the individual’s situation—the extent to which fixed expenses are covered by nonportfolio income sources.

Ju mer jag läser om SWR, desto mer landar jag i att det “beror på” Jag tror helt enkelt alla måste göra upp med sitt och komma fram till vad som är min SWR än att det finns någon typ av sanning.

Morningstars artikel är ju lite att fila på detaljerna men kanske att missa big picture. Bengens “ungefär 4%” för 30+ år sedan blir 3.8% i denna artikeln för 2022. Dessutom att det ifjor var 3.3%? 15% skillnad i uttaget bara på 1 år. Just pga detta landar jag i att man får göra sin egen bedömning. Mycket beror dessutom på det året man “går” så att säga hur mycket SWR egentligen är rimligt.

Lyssnade också (tyvärr) på Rational Reminders avsnitt 229 - länk nedan. Fick tipset här på RT men kommer inte ihåg av vem (sorry). Kan varmt rekommendera det. De landar i 2% SWR eftersom de menar att de 4%en:ish är typ dopade av att vara framtaget för amerikanska marknaden, ett land där inga riktiga katastrofer hänt, marknader inte gått helt åt pepparn, valutan inte kollapsat mm. De lyckas logiskt leda fram att om man räknar med att råka för katastrofer i snitt så blir det mer 2%. Min tolkning av deras resonemang

Gigantisk skillnad 2-4% i vilket kapital man behöver

Så jag tänker

Utgångsläge 3-4%, gärna närmare 3%

För att hantera kris/ras på ens tillgångsvärde situationer - räkna ut hur mycket man kan dra ner kostnaderna i pension/FIRE - ett scenario med “helt OK” levnadsstandard utan guldkant - ett scenario “bare minimum” typ mat och tak över huvudet

Om scenario 1-2 landar på mindre än 2% uttag av kapitalet så borde det vara ok.

Alltså ett mer dynamiskt tänk än X% av kapitalet och sedan inflationsjustera uttaget.

Också lyssnat på den och det de säger är ju vettigt. Speciellt om man har en stor home bias. Många länder som råkat illa ut senaste 120 åren med alla krig etc.

Så långsiktigt tänker inte jag. Målet är jobba minst till 65. Den dag när jag lägger av med jobbet då får det bli vad det bli av det hela. Bara anpassa sig efter situationen. Vi människor är ganska duktiga på att överleva . Leta pantburkar ger ändå lite gratis motion även när man blir gammal . Man får vara glad att man har upplevt till 80+ och fortfarande så pigg att man orkar leta efter pantburkar

Fast här handlar det ju inte om att maximera avkastningen, utan om att kunna få en hyfsat säker ström av pengar som man kan leva på. Väldigt olika målsättningar.

While we can never know what the safe withdrawal rate will be in the future, we can solve for what the safe withdrawal rate has been in the past. With this in mind, I tested withdrawal rates ranging from 4% to 10% on portfolios ranging from 50% U.S. stocks/50% U.S. bonds to 100% U.S. stocks/0% U.S. bonds. Overall, the results led me to three conclusions:

Despite having more historical data (through 2022), the safe withdrawal rate is still 4%.

If you can get by with a lower withdrawal rate (<6%), you portfolio should own a decent amount of U.S. bonds (30%-40%).

If you require a higher withdrawal rate (>=6%), then you should allocate more to U.S. stocks (80%+), which will decrease the chance that you run out of money in retirement.

Note: Requiring a higher withdrawal rate is riskier in that you are more likely to run out of money in retirement. However, if you must withdraw more, then it’s actually less risky to invest in assets with higher expected returns (i.e. stocks over bonds). Why? Because this additional growth is the only chance you have of not running out of money with such a high withdrawal rate.

While these results might seem at odds with each other, they actually aren’t. Since U.S. stocks have had many periods of high growth and a few rare periods of low/negative growth, they tend to be your best option for most of your portfolio most of the time. Let’s look at some results to illustrate this.

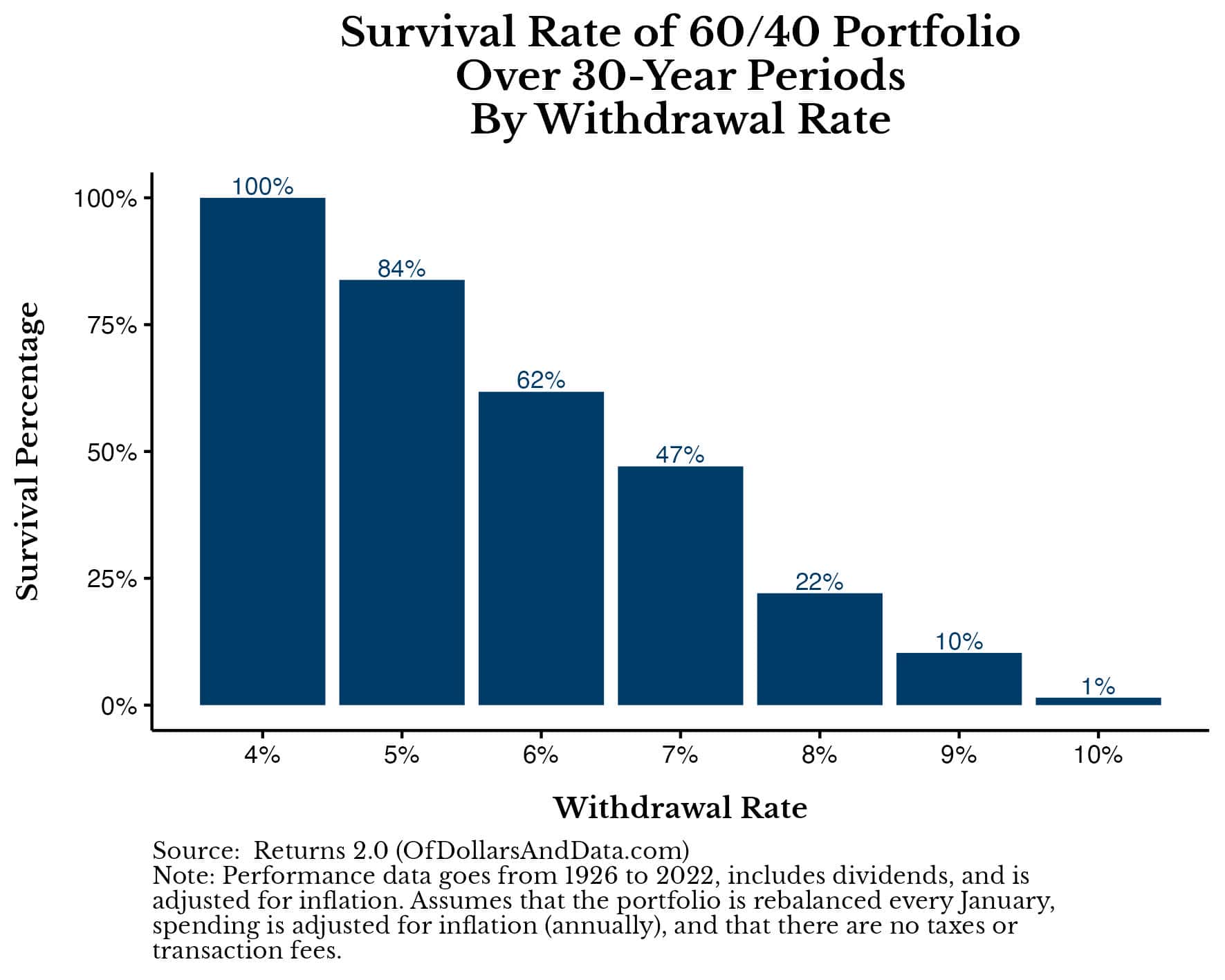

To start, we will examine how a 60/40 portfolio performed with various withdrawal rates across every 30-year period from 1926 to 2022 (68 full periods in total):

As you can see, while this portfolio does well with a 4% withdrawal rate (surviving 100% of all 30-year simulations), as you increase the withdrawal rate, the rate of failure also increases. As a reminder, in all of the simulations I ran your spending is set at the very beginning of the simulation (Year 1) and then adjusted annually by inflation each year for the next 30 years.

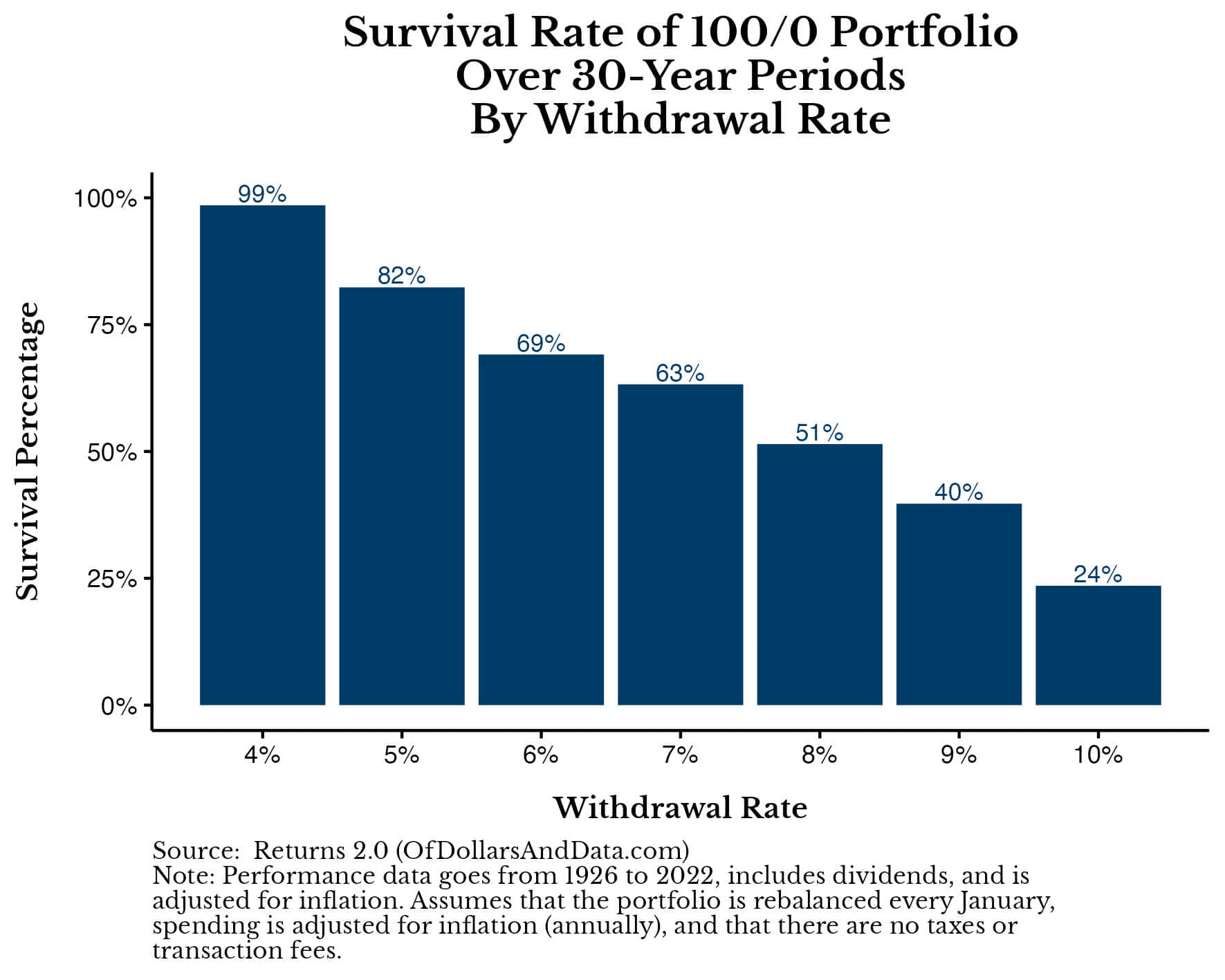

We can compare this to using a 100/0 (“All Stock”) portfolio and see that the All Stock portfolio performs much better at higher withdrawal rates:

Now, with a 100% U.S. stock portfolio, your chance of survival with an 8% withdrawal rate would’ve been greater than 50% compared to only 22% for a 60/40 portfolio. This is because these 51% of simulations all correspond with historical periods where U.S. stocks had incredible growth without deep, extended downturns. Overall, these suggests that, when you must withdraw more, you need to take more risk to accommodate this higher need from your portfolio.

But instead of just examining these results in a vacuum, I’ve also created a GIF that cycles through these results (from a 50/50 portfolio to a 100/0 portfolio) so you can compare them visually more easily:

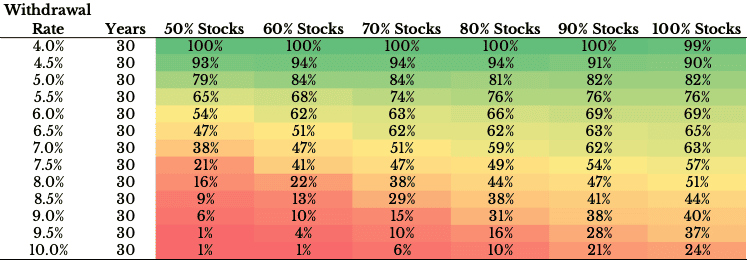

This makes it easier to see how much of a benefit you get by relying on a higher stock allocation when requiring a higher withdrawal rate. In addition, I also created a heatmap of these results where you can compare all of these portfolios and their survival probabilities at once (for various withdrawal rates):

The green section across the top represents the safe withdrawal rate, where you would not have run out of money in nearly all historical periods. But as you move down the table (by increasing your withdrawal rate), the results become increasingly worse as you become more likely to run out of money.