Spelar ingen roll om man sysslar med stockpicking, folk med fonder presterar inte heller så bra.

Exempel 1: Folk blir rädda när marknaden går ner, dvs säljer lågt och köper högt.

Peter Lynch, who formerly managed the high-flying Fidelity Magellan Fund from 1977 to 1990, is a legendary investor. Under his management, the fund averaged an astounding annual return of 29%. It would seem all you had to do was ride along with Lynch and you would earn phenomenal returns. But that didn’t happen. According to Fidelity Investments, the average Magellan Fund investor lost money during Lynch’s tenure there.

– How Investors Are Costing Themselves Money

Här pratar vi alltså folk med likadan portfölj, men där småsparare får mycket lägre avkastning än själva fonden.

Exempel 2: Folk jagar vad som presterat bra på sistone, men kommer in för sent.

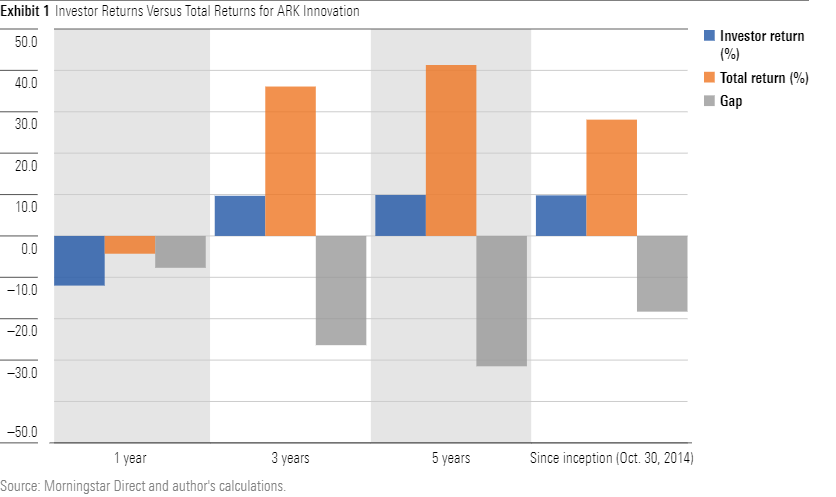

Alla hade ögonen på Cathie Woods (ARK Innovation) senaste åren eftersom hennes fonder gick sjukt bra. Tyvärr kommer småsparare in sent och får knappt någon avkastning på sitt höga risktagande (avkastningen är jämförbar med S&P index, vilket har mycket lägre risk än en enskild fond).

– https://www.morningstar.com/articles/1071658/arkk-an-object-lesson-in-how-not-to-invest

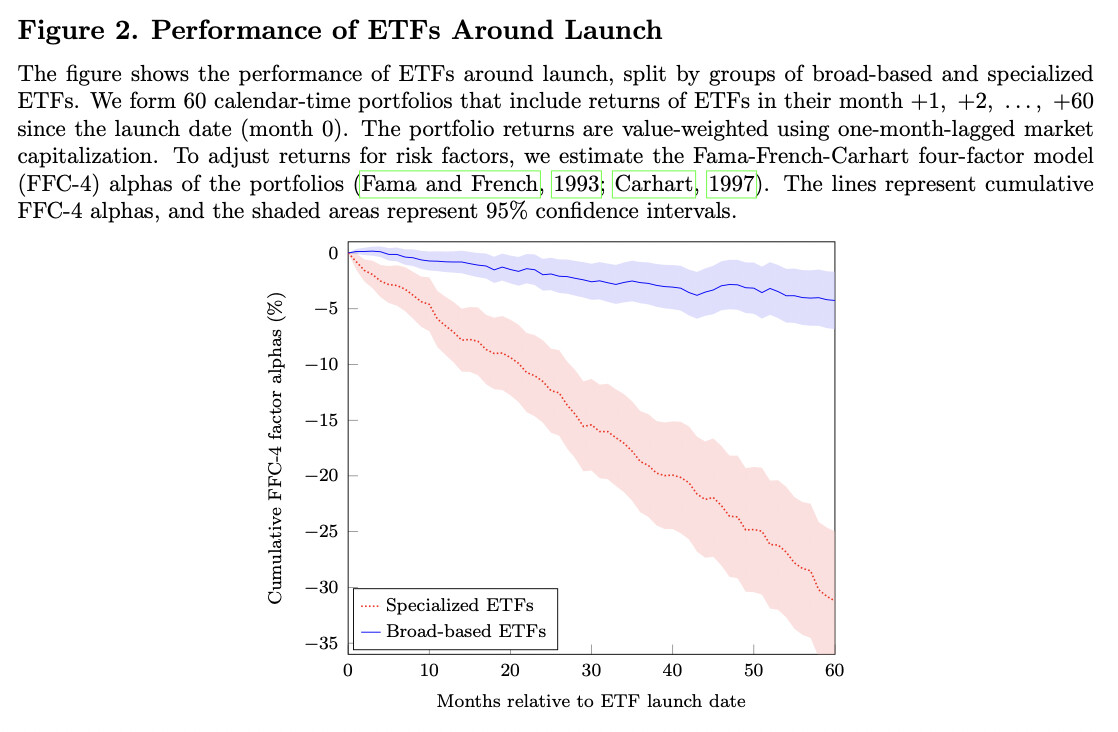

Ett annat exempel. Folk gillar branchfonder, men går ofta in när uppgången i branchen redan skett.

In fact, we find that the performance of special- ized ETFs is disappointing in terms of both raw and risk-adjusted returns. A portfolio of all specialized ETFs achieves risk-adjusted returns of −3.1% per year, after fees. This underper- formance is due mostly to recently launched specialized ETFs, which grossly underperform: about −6% annually in the first five years after inception. In comparison, the performance of broad-based ETFs is slightly negative, though statistically indistinguishable from zero. The underperformance of specialized ETFs is not explained by their higher fees, as it persists in terms of gross returns. The absolute size of the underperformance of specialized ETFs is nonnegligible in dollar terms given that the assets in these funds are sizeable—about $460 billion at the end of our sample. Figure 2 illustrates this result.

– https://www.nber.org/system/files/working_papers/w28369/w28369.pdf

synd att avanza bara gav akitesiffror för ett år, skulle vilja se hur det ser ut över 5-10år eller mer och fler detaljer, som hur många som ens når avkastning motsvarande brett svenskt eller globalt index över mätperioden.

synd att avanza bara gav akitesiffror för ett år, skulle vilja se hur det ser ut över 5-10år eller mer och fler detaljer, som hur många som ens når avkastning motsvarande brett svenskt eller globalt index över mätperioden.