Ny diskussion utifrån tråden “Invändning mot indexfonder: det är en risk med den stora koncentrationen till de få stora bolagen”. Denna diskussion handlar fördelar och nackdelar med att välja ett index där alla bolagen har samma vikt istället för att de väljs baserat på hur stora de är.

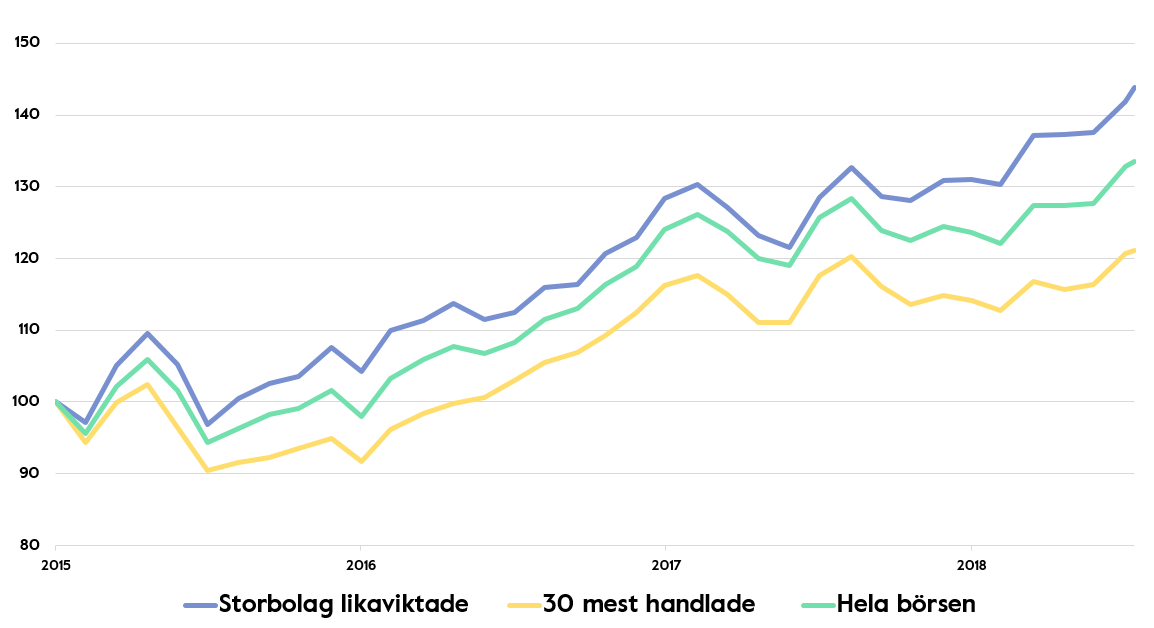

Det kan finnas anledningar till att likavikta som grafen visar kan man få högre avkastning om man gör det. Tänk när Ericson utgjorde 40% av omxs 30 år 2000 det är väldigt hög risk enligt mig. Likaviktat hade Ericson varit 3,3% av omxs 30 då hade man klarat it krachen bättre och fått en bättre sharpekvot. Eller 1989 när ett japanskt index innehöll 80% bank och finans.

Skulle säga att detta är felslut. Genom likavikt överexponerar du relativt marknaden småbolag. Då är du med på fler resor upp för små bolag tills de växer i storlek och därmed tar del av den intiala aggresiva uppgången för ett litet antal bolag. Dessa som är den skevness du talar om.

Det skulle i så fall öka risk och avkastning. Vilket också är konsekvent med riskfaktorn småbolag.

2 gillningar

Hmmm… jag är inte helt övertygad för jag överviktar ju alla andra också, inte bara småbolag. Jag får fundera och återkomma… Låt oss göra det till en egen tråd. ![]()

Pratar vi om absolutavkastning eller riskjusterad avkastning?

Pratar vi riskjusterad avkastning så skulle likaviktad kunna underprestera, även om den sedan 1970 presterat lika som marknadsviktat (mätt i sharpe iaf).

Pratar vi absolutavkastning har ju likaviktat varit det klart bättre valet, mestadels på grund av storleksfaktorn.

Ja, och de största vinnarna (i procent) brukar vara småbolag.

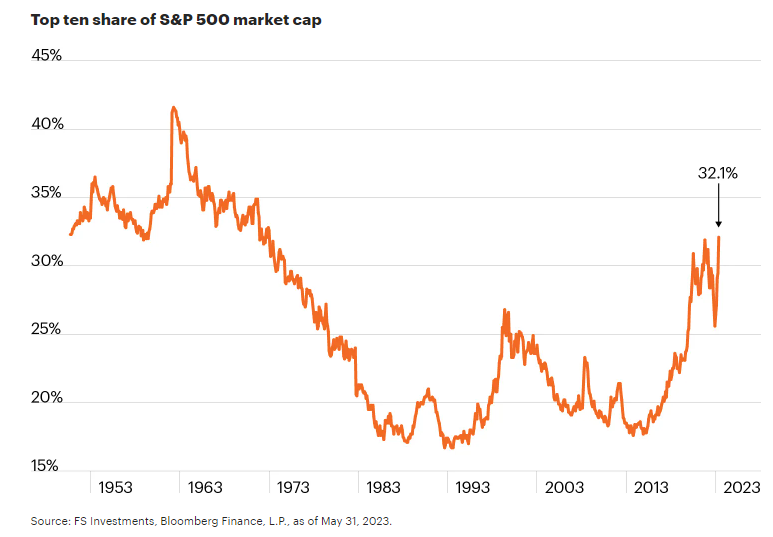

Du skapade t.ex en tråd där du noterade att “tre aktier (Nvidia, Microsoft och Apple) stod för hälften av uppgången i S&P500 i 2023Q1”, men jag påpekade då att 24 bolag avkastade bättre än Apple och 40 bolag avkastade bättre än Microsoft i procent.

Som investerare bryr vi oss inte om hur mycket ett bolags börsvärde stiger i dollar, utan bara i procent!

Ja, likaviktat underviktar momentum, men överviktar å andra sidan då lite värde.

Sälja av vinnare och köpa förlorare kan också generera en liten positiv ombalanseringseffekt.

Riskpremien är högre för likaviktat (storleksfaktorn), vilket höjer dess förväntade avkastning.

Vilka “alla andra” pratar vi om här? Inte säker på vad du menar.

3 gillningar

Tänkte främst large och midcap samt small cap blend /growth dvs inte bara small cap value.

Att övervikta small cap growth är inte optimalt, det är sant, men det övervägs av att mid cap och small cap value kan förväntas vara klart bättre än large cap när det gäller absolutavkastning.

Intressant nog så har mid cap varit bättre än small cap sedan 1972 (på grund av hur dålig small cap growth har varit).

2 gillningar

Från Bogleheads wiki:

The investment performance of an equal weight stock index will be affected by its greater holdings of smaller companies, any value tilt the weighting brings to the index, and the effects of quarterly rebalancing.

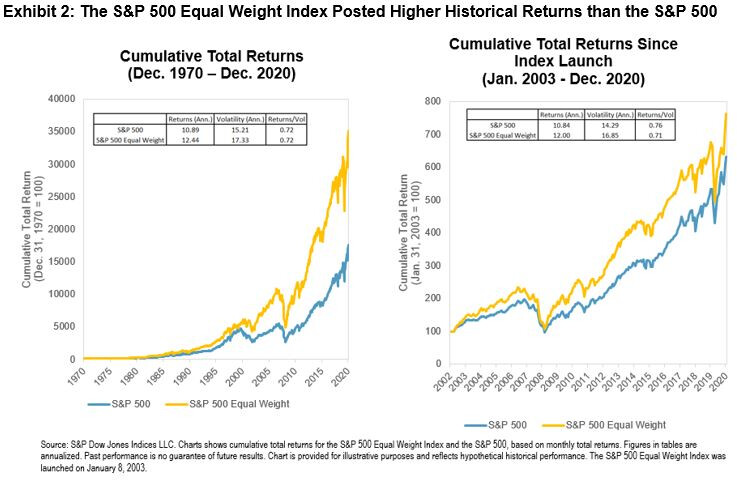

S&P has back-tested results for the S&P EW 500 index going back to 1990 (the index was created in January, 2003.) Over the (1990 - 2009) period, the compounded annual return of equal weight 500 index outperformed the cap weight 500 index by +1.8%, but with considerable variance over market cycles.

S&P reports that the EWI would have outperformed the S&P 500 in the early nineties; underperformed during the 1994 - 1999 period dominated by technology growth stocks; and outperformed over the 2000 - 2009 period. The S&P EW index tends to have higher volatility than the S&P 500.

Over the 2002 - 2007 period the annualized standard deviation was 10.97% for the S&P EWI versus 8.61% for the S&P 500. Correlation of the S&P EW Index to the S&P 500 Index ranged from 84% to 98% (1990 - 2009), with the lowest correlations occurring during the 2000 - 2002 bear market.

The following table provides annual returns for the S&P EWI.>

S&P Equal Weighted 500 Index Returns

Year S&P EW 500 TR S&P 500 TR 2018 −7.64% −4.64% 2017 +18.90% +21.83% 2016 +14.80% +11.96% 2015 −2.20% +1.38% 2014 +14.49% +13.85% 2013 +36.16% +32.39% 2012 +17.65% +16.00% 2011 −0.11% +2.11% 2010 +21.91% +15.05% 2009 +46.31% +26.46% 2008 −39.72% −37.00% 2007 +1.53% +5.49% 2006 +15.08% +15.79% 2005 +8.06% +4.91% 2004 +10.88%

Här är en riktigt bra tråd på ämnet från Bogleheads där de diskuterar fonden RSP som är en likaviktad S&P500-fond.

Några höjdpunkter (min fetstil):

It is normal for the stock market to be dominated by a few large companies, that’s just the way it is. And usually the companies that are at the top have a good deal of faddishness, bubbliness, and irrationality to them, and that’s just the way it is, too. And the odd thing is that the “fundamental indexing” products that specifically seek to avoid participation in the craziness have been out for well over a decade, and haven’t proved to perform all that differently from cap-weighted products.

Let’s not argue about which is better , the S&P 500 fund (orange) or the Schwab Fundamental US Large Company Index Fund (blue), let’s just observe that top-heavy or not, the S&P 500 fund just didn’t stink all that badly.

In fact, despite trying to avoid the fundamentally unsound companies, the fundamental-weighted fund actually took deeper dives in 2008-2009 and this year. And the same thing held true for RSP (green).

You’d think trying to stay out of the craziest stocks would moderate volatility, it sounds like it would do that, but it hasn’t done that.

och

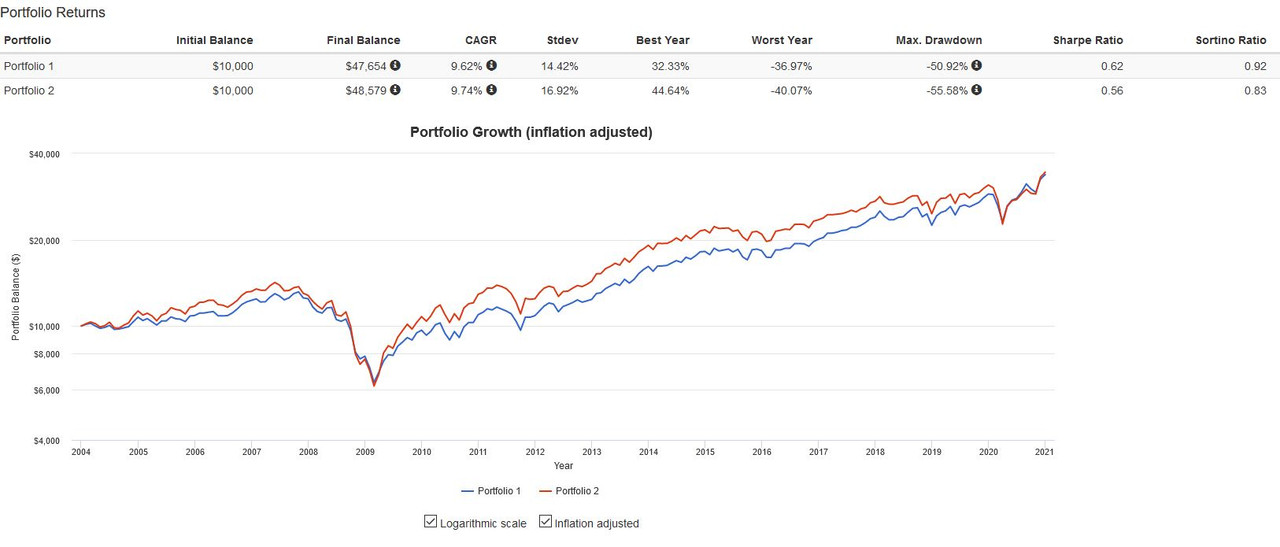

while RSP (=equali weight) had slightly better CAGR (9.74% vs 9.62%) it had LOWER risk adjusted returns per sharpe and sortino ratios. It had higher standard deviation too.

whatever gains it had over S&P starting 4/30/2009 gave it up by 3/31/2020. So the 10 year outperformance was lost in year 11. It started ahead again, but only around 11/30/2020 and there’s no guarantee that will continue and if it does, how long? How patient are you?

markets are generally dominated by a few companies. Only 4% of all companies have created the value of the market since 1926 (source: https://papers.ssrn.com/sol3/papers.cfm … id=2900447)

The four most dangerous words in investing are “This time is different”. Sir John Templeton

samt

If two companies in the S&P 500 merge, RSP will cut its exposure to the combined business in half. Does that make sense?

If an S&P 500 company spins off another company big enough to be in the S&P 500 company, RSP will double its exposure to the split businesses. Does that make sense?

Market cap investing gives us an equal share of all businesses, for which we must pay the going rate. So-called “equal weight” investing says we ought to buy an outsized share of smaller businesses. This incurs trading costs and is unlikely to yield a higher long run return. And if you believe in the size factor, there are more efficient ways to get it.

Från en annan tråd:

As for RSP, the statement that it “provides a better risk/return profile than total market” is factually incorrect. It just hasn’t been so.

RSP has had slightly higher return (CAGR), but higher risk by standard deviation and other measures–as you’d expect because equal weighting is a small-cap tilt relative to the market. By two standard measures of risk-adjusted return, the Sharpe and Sortino ratios, the total market has had a better risk-adjusted return.

If you go in yourself and set the end date to 12/31/2019 you’ll see that even if you exclude 2020, the risk-adjusted return was still (microscopically) higher for VTI.

samt

Market Cap Weighted is the cheapest and most available. Although it doesn’t show up as having a momentum factor (because it is considered the reference point) it does, because it systematically holds more stocks and sectors with high market caps. It also tends to hold a disproportionate amount of large cap stocks.

Equal Weight has higher volatility because of its higher exposure to small and value stocks. However, it essentially has negative exposure to momentum because it rebalances often (and rebalancing is most effective when done less frequently because it takes advantage of momentum). On the flip side, Equal Weight’s higher volatility improves returns with accumulation portfolios and when it’s rebalanced against bonds or international stocks. But, of course, volatility is not desirable for distribution portfolios.

Sector Equal Weight, like standard Equal Weight has less momentum and less large cap allocation than Market Cap does, but actually has lower volatility. However, there seems to be more idiosyncratic risk because you’ll have about 50% of your money in sectors that respectively make up 2 or 3% of the market by capitalization.

2 gillningar

Vissa bra insikter, men problemet med den data de diskuterar är att det är så begränsad historik.

Det mesta av grafen består ju av tiden 2010 - 2021 som var en av de bästa perioderna för stora tillväxtbolag någonsin.

Titta på min graf där uppe som sträcker sig tillbaka till 1970 för längre perspektiv.

Det största problemet med equal weight är bristen på tillgänglighet.

Xtrackers SP500 equal weight finns för 0.11% avgift, men de flesta av oss vill ju ha något mer bredare.

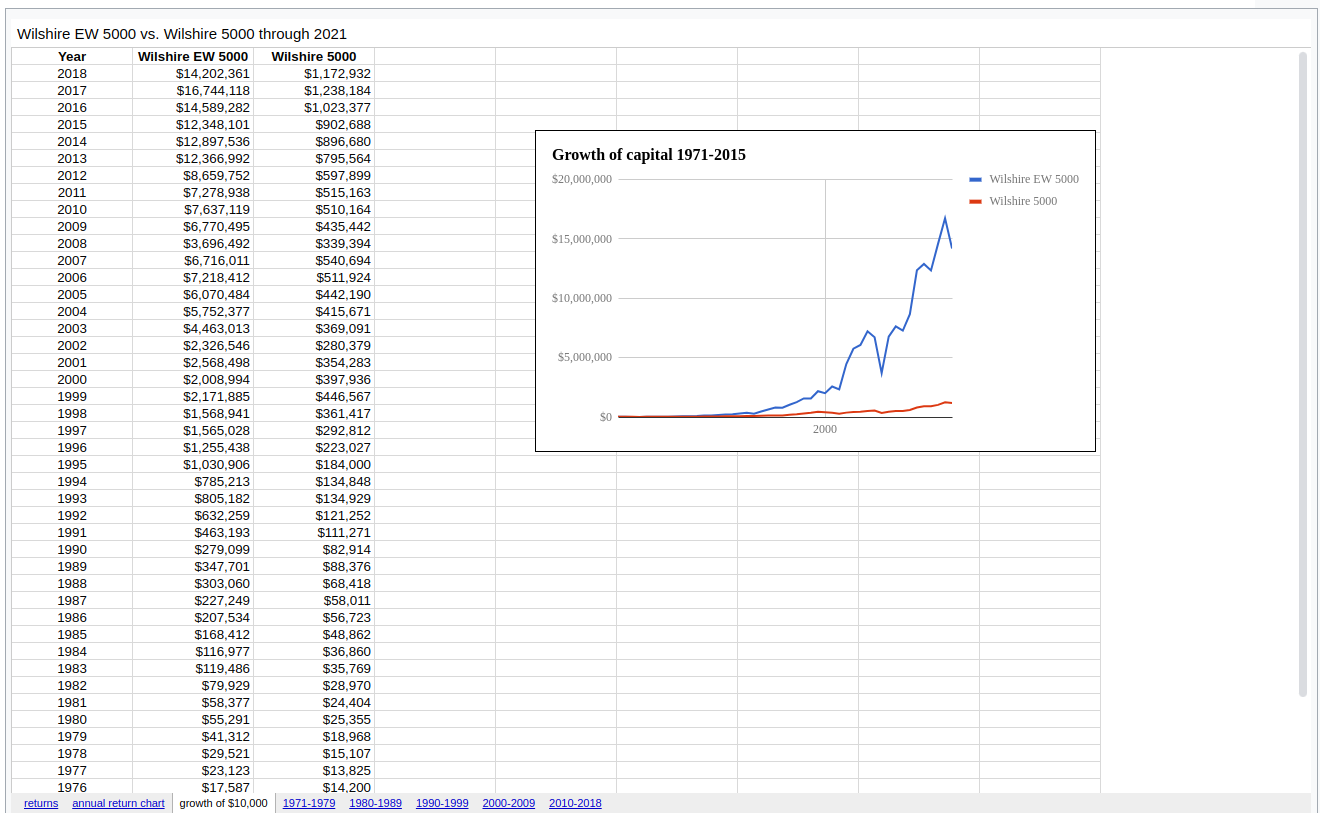

Hittade nu en ännu mer förkrossande graf från Bogleheads wikin!

Om du år 1971 investerade $10,000 i Wilshire 5000 så hade du år 2018 haft $1,172,932.

Hade du investerat i Wilshire 5000 Equal Weight så hade du haft $14,202,361!

(Sen måste man såklart ta avgifter i beaktande, men ändå…)

Men jag blev inte klok på om den gick att köpa?

Det jag upplever att folk klagar på är att SP500 EW beter sig som en SP500 midcap-fond.

The fact is that the bottom 300-400 stocks in the S&P 500 behave much more like mid-cap stocks than they do like large cap stocks, and the majority of the weight of RSP is on those stocks.

You will be much better served by relying on the ACTUAL performance of the relevant funds than on the marketing material that Invesco is supplying. Take a gander at a plot of the first two principal components of the oldest low-cost so-called “large cap” and “mid cap” funds. This is based on 15 years of monthly returns, and these first two PCs explain 99.1% of the variance of these funds. What do you see?

I’ll tell you what I see.

The funds represent a range of behaviors, and roughly form an axis from upper left to lower right. The northwest-most fund is the Invesco S&P 500 Top 50 ETF (XLG) and the southeast-most fund is the Vanguard Extended Market ETF (VXF).

The large cap funs (in blue) are far from a homogenous bunch, occupying a range of market cap exposures.

There’s a surprisingly clean break between the funds Morningstar call “mid cap” (orange) and “large cap” (blue), with one notable exception.

The notable exception is shown in red and it is, as you should have guessed, Invesco S&P 500 Equal Weight ETF (RSP).

I think it’s hard to argue that it’s ACTUAL performance is not that of a mid-cap fund. You could make the cast that it behaves like the biggest mid-cap fund in this sample, but there’s not doubt that what you’re buying is a mid-cap fund.

Scooter57 wrote: ↑Thu Jan 14, 2021 7:40 pmI don’t want to buy a mid cap fund instead of a large cap fund.

I’m not suggesting that you should buy a mid-cap fund instead of a large cap fund. Obviously, you should do what you want.My intent is merely to help you understand that RSP actually behaves like a mid-cap fund .

If that’s what you want, there are much cheaper funds that provide the same “doesn’t put all my money into Amazon, Tesla, Facebook, and Google” result.

If that’s NOT what you want, then don’t buy RSP.

1 gillning

Att equal weight beter sig som mid cap är väl “a feature, not a bug”?

Det är ju denna lutning mot mindre/medelstora bolag som man vill åt i en EW,

utan att för den skull helt exkludera de största bolagen (“köp hela höstacken”).

Enligt den andra grafen jag postade där uppe så har ju mid cap gett bättre avkastning än både large cap och small cap sedan 1972, så att den beter sig som mid cap är väl knappast något negativt ![]() .

.

Han säger att mid cap är billigare än equal weight, men vad jag ser så kostar SP400 mid cap 0.3%, medans sp500 EW alltså kostar 0.11% (0.2% om man vill ha icke-ESG verkar det som).

1 gillning

Men finns det något egenvärde i att ha just jämvikt? Om EW-index bara är en halvdassig proxy för att komma åt andra faktorer, som t.ex. små- och värdebolag, så kommer det ju aldrig vara en optimal lösning för någonting.

4 gillningar

Jag personligen kommer nog inte investera i något EW-index, men argumentet jag kan se är om man vill luta mer mot mindre/medelstora bolag, men samtidigt fortsätta investera i “alla bolag”.

1 gillning

Upplever från ovan att det vore nästan bättre att då köra mer “rent” genom t.ex. SCV som jag upplever mer stöd för än en midcap-fond.

1 gillning

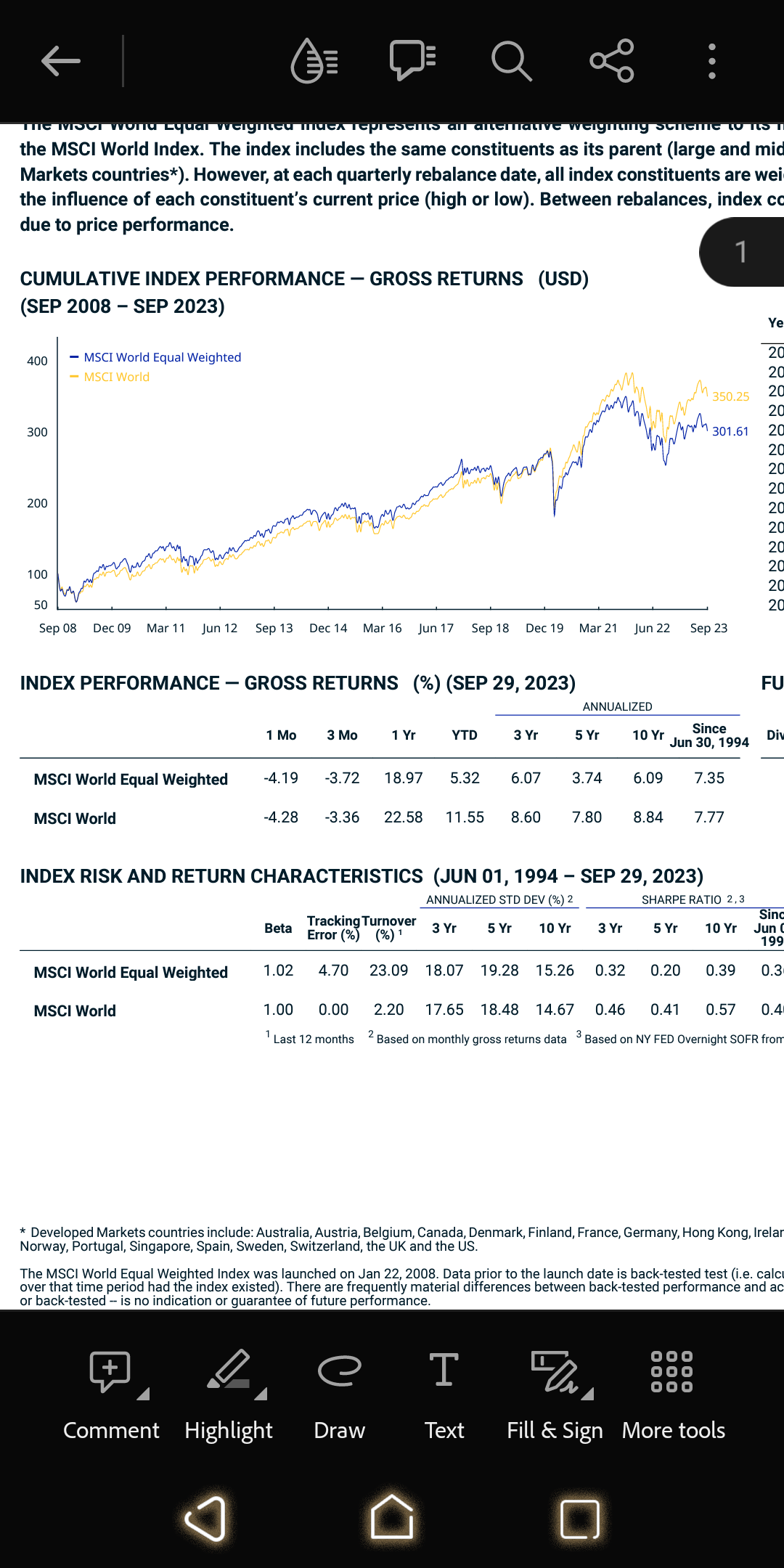

Msci World Index Equal Weighted har underpresterat MSCI World Index sedan 1994.

https://www.msci.com/documents/10199/f7972c87-76f7-425b-9942-4e8929255210

2 gillningar

Ursäkta, men jag fartar ingenting. Om man har ett rent index och ett företag drar i väg, så är man ju som fondägare med på hela uppgången. Se på exempelvis HM som gick från några få procent till 10 procent av Stockholmsbörsen.

Missuppfattningen för många är sedan att man på något konstigt sätt tror att fördelningen gäller i all framtid. När HM sjönk skulle man därför ha förlorat hela uppgången. Så är det ju inte alls.

Tack vare den regelbundna OMBALANSERINGEN kommer nedgången att dämpas. Nedgången kom ju direkt inte över en natt. Dessutom kommer de aktierna som köps i stället att gå bra i de flesta fall.

Att ha ett korrigerat index hade gjort att man inte varit med på uppgången, så jag ifrågasätter starkt om detta hade varit bättre.

2 gillningar

Du är alltså med på nergången också, precis i samma utsträckning som du är med på uppgången…

Är detta verkligen en vettigt diskussion? Är det utveckligen av respektive index inte beroende av vad det består av? Har vi en koncentrerad marknad så blir ju skillnaden mellan indexen större. Därtill så kan ju olika brancher och ha olika stor del i olika index i olika länder. Tittar man på de största bolagen i USA så är det techbolag tex. Skillanden i utfall mellan market weight och equal weight beror just på detta och är bara en slumpmässigt proxy för kompositionen i respektive index ser ut. Min poäng är att det är svårt att hitta data som är jämförbar över då då kompositionen ändrar sig.

Vi kommer alla att dö. Inget sparande är för evigt. Ingen vet när det är dags att köpa eller sälja med maximal effekt.

Den som gick in tidigt och köpte HM fick en rejäl skuts uppåt. Den som gick köpte på topp drabbades av motsatsen.

Att försöka “justera” marknaden till sin fördel är minst sagt svårt. Titta hur det har gått för Aktiespararnas Direktavkastningsfond de senaste åren. En rejäl flopp.